| Home | Revision | A-Level | Economics | Managing the Economy | Gross domestic product (GDP) |

Gross domestic product (GDP)

What is the gross domestic product?

The GDP is the value of all the goods and services produced within a country, usually measured over one year.

How do we measure GDP?

There are three ways of measuring: By output, by expenditure, or by income. All three methods should give same result.

Why do we get the same result? Because producers have to pay to get the materials and workers they need (so they receive an income); then what is produced is bought by someone (consumers or wholesalers = expenditure; to make it easier to understand we assume that all is sold, although this is not actually necessary); and what was produced of course is output. So income = expenditure = output.

Incomes consist of wages, interest, rent, and profit.

Note that profit always adjusts to make incomes equal output. Why?

Consider this. If we pay out £90 to make an item (it goes as income to someone) and then we sell it for £100 (which is expenditure), it means that profit is £10.

But we know that incomes + profit (£90 + £10) = £100

And we know that expenditure = £100

Therefore the two are the same.

So incomes must equal expenditure, as profit is always the difference between the two. Take another example. Suppose we buy for £90 and find that we can only sell it for £85?

We still have £90 going to someone as income, but an expenditure of only £85. There is a loss of £5. So either profit or loss adjusts to make incomes identical with expenditure. And of course, a loss is merely a negative profit!

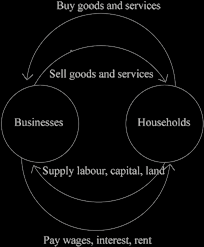

See the diagram below which shows all the flows in domestic national income.

You might see this diagram representing the nation’s production/income/expenditure sometimes called “the wheel of wealth”.

It excludes foreign trade (imports and exports) as this refers only Gross Domestic Product. We can easily add these two extra flows, but why complicate things? If we chose to do add these flows, the diagram would then represent Gross National Product as we would be considering the whole nation, not just domestic production.

Some technical problems when adding up the GDP

For incomes, we must exclude transfer payments (they are not a reward for producing anything) like old age pensions or child support.

For output, we must avoid double counting, e.g., we take just the price of a loaf of bread, not the value of the wheat, flour, transport and storage costs in addition; they are already included in the final price, as the retailer sells at a price that covers all his or her earlier costs!

We use value added at each stage to avoid double counting.

For expenditure, we take the market price but we must remove VAT and other taxes which the government has put on as an extra; and we add in any subsidy government has paid, to get the true price are seeking.

Because there are so many items to find and add up, the three methods are never quite identical in practise – in the real world there is a statistical discrepancy (people make mistakes in recording, there are time lags in pieces of paper moving

about, some get lost and so forth) and we use a “balancing item” to make the figures exactly the same. It is usually quite small.

“Gross Domestic Product” and “Gross National Income” (GNI)

GNI is obtained by adding foreign-earned incomes from property owned abroad or employment abroad to GDP (remember that “income” is the “I” bit of “GNI”).

“Gross National Income” and “Net National Income” (NNI)

To obtain net national income we subtract a percentage from gross national income to allow for capital which wore out or became obsolete in the year we are looking at. In short, to get from gross to net, we make an allowance for the depreciation of capital.

It may seems complex but all you have to remember is:

“Domestic” means no foreign sector is included.

“Gross” means no depreciation for capital has been made.

“Product” means output, and excludes incomes coming from (or to) abroad. “Income” means we do include foreign income flow.

We can combine these words to get different measures.

We chose the measure we need to answer the question we are asking.

The simplest is GDP, it is the one that is most used and you will encounter, and it is the easiest to find for more countries.